Non-residents in Spain who own real estate in Spain are subject to Non-Resident Income Tax (IRNR).

Let us see below in which cases non-residents will have to pay this tax, when and how much:

a) Rental of housing

If the non-resident rents the property, he/she will have to pay tax on the income from said property, i.e. on the income or rents received. In the case of residents of an EU country, Iceland or Norway, the tax rate will be 19% of this income. For residents of any other country the tax rate will be 24%.

Owners resident in the EU, for example in the Netherlands, who rent out their property will be able to deduct expenses in proportion to the length of time the property has been rented. On the other hand, owners who are NOT resident in the European Union or the European Economic Area must be taxed on gross income (they are not allowed to deduct expenses) and will pay 24%.

The declaration of rental income must be submitted at the end of each quarter, i.e. during the first twenty calendar days of April, July, October and January, in relation to the income that the non-resident owner received in the previous calendar quarter.

In the case of a double taxation agreement with Spain, the owner of the property may deduct the amounts paid for this tax in the income tax return to be filed in his country of tax residence.

b) Empty or owner-occupied housing

If the property is empty or for own use, non-resident owners will have to pay tax on the hypothetical income generated by the own use. The tax rate will also be 19% for residents of the European Union, Iceland or Norway and 24% for residents of other countries. In both cases the tax is calculated on the basis of 1.1% of the cadastral value of the property if this value was revised after 1 January 1994 or 2% in other cases.

Example: Dieter Schmidt, resident in Germany, is the owner of a flat in Altea which he uses for his holidays and whose cadastral value is 250,000 €. The basis of calculation is 250.000 x 1,1% = 2.750 €. The tax rate will be the result of applying 19% to 2.750 €, i.e. 522,50 €.

The period for filing and payment of the non-resident income tax in the case of property intended for own use will be between 1 January and 31 December of the year following the year in which the tax accrued. In general, the gain will be determined by the difference between the acquisition value and the transfer value, and the tax rate will be 19% of this gain.

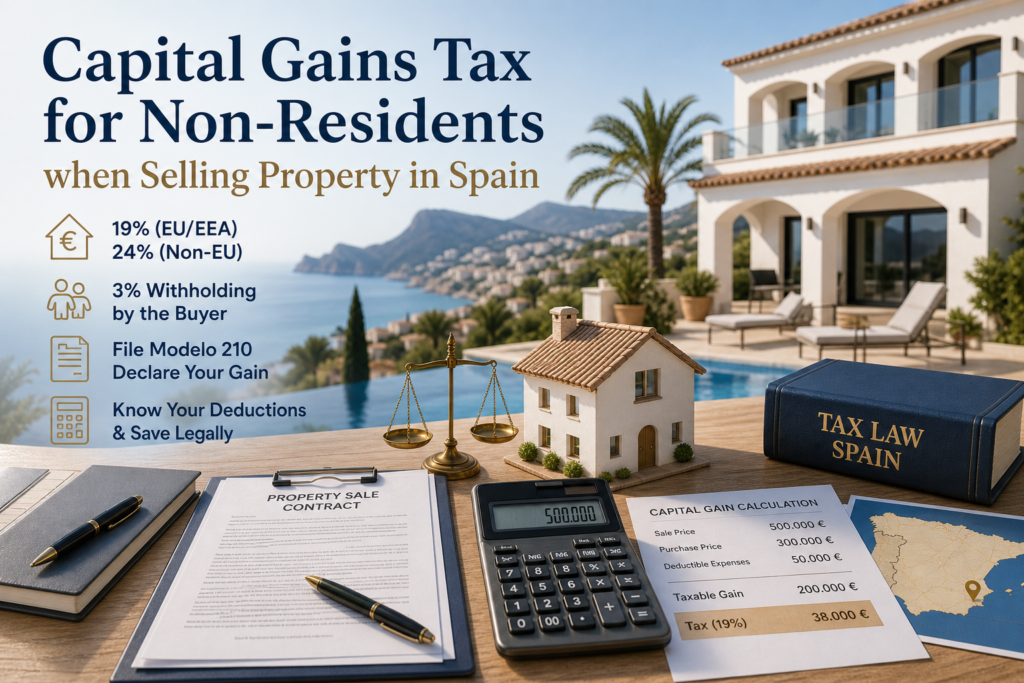

c) Sale of the property

Within a maximum period of three months from the sale of the property, the non-resident owner must declare his gain and pay the corresponding tax.

The person who buys a property from a non-resident, whether resident or non-resident, will be obliged to withhold 3% of the price and pay it to the tax authorities.

This payment made by the purchaser of the property will have the character of a payment on account of the tax payable by the owner-seller on his gain. In the event that the 3% paid by the buyer is higher than the amount that the owner-seller must pay, he/she will be able to obtain a refund of the excess.

What happens if the buyer does not pay the 3%? In this case, the property purchased will be subject to the payment of the tax and the Land Registry will record this in the registration of the property in favour of the purchaser. And this annotation will only be cancelled by expiry, by means of the presentation of the payment letter or administrative certification that accredits the non-application or the prescription of the debt.

ATTENTION!

The Spanish Tax Authorities do not send non-resident taxpayers any communication, payment notice or settlement relating to Non-Resident Income Tax, but non-residents (or their representatives) are obliged to make the calculation, complete the corresponding self-assessment form and manage the payment of the tax.

It is important to warn property owners who have not filed a Non-Resident Income Tax return that they should regularise their tax situation in order to avoid significant financial penalties.

It is also important to clarify that non-residents who own a property are not only obliged to file a tax return for the ownership of that property but also for any other income obtained in Spain through economic activities.

How Inheritance Works for Foreign Property Owners in Spain

A Strategic Guide for International Property Owners on the Costa Blanca For many international buyers,…

What Is an “Out of Planning” Property in Spain — Can It Be Sold?

If you own or are considering buying a property in Spain,particularly in areas such as…

Capital Gains Tax for Resident Foreign Homeowners

A clear guide for resident property owners in Altea and the Costa Blanca For many…